Fred Thompson checks in with another post on IP28.

Over

the next 3 months, proponents and opponents of this Measure will make a lot of

wild, unsubstantiated claims about what it will or won’t

do.

My purpose it to try to distinguish sense from spin, as honestly and objectively

as I can. Frankly, this is not easy. Not only because IP28 is unlike anything

found in the public finance universe and is, therefore, extremely hard to parse,

but also because it appears to be nearly everything a good tax is not. Tax

experts believe that good taxes should treat the things being taxed more or

less equally, that they should be fair, broad based, transparent in incidence

and effects, and straightforward in administration. IP28 is unequal, probably regressive,

narrow, opaque, and likely to encourage further avoidance. Consequently, every

fiber of my being as student of public finance wants to say it’s spinach, to Hell

with it. But I’ll do the best I can, starting with claims made about the

existing tax system.

Proponents

of IP28 claim that “Oregon has the

lowest corporate taxes in the country.” What that means to an economist

is that Oregon ranks dead last in corporate income tax (CIT) collections or

that the growth of its CIT collections have lagged those of all other states.[1] Clearly,

neither of those claims is true.

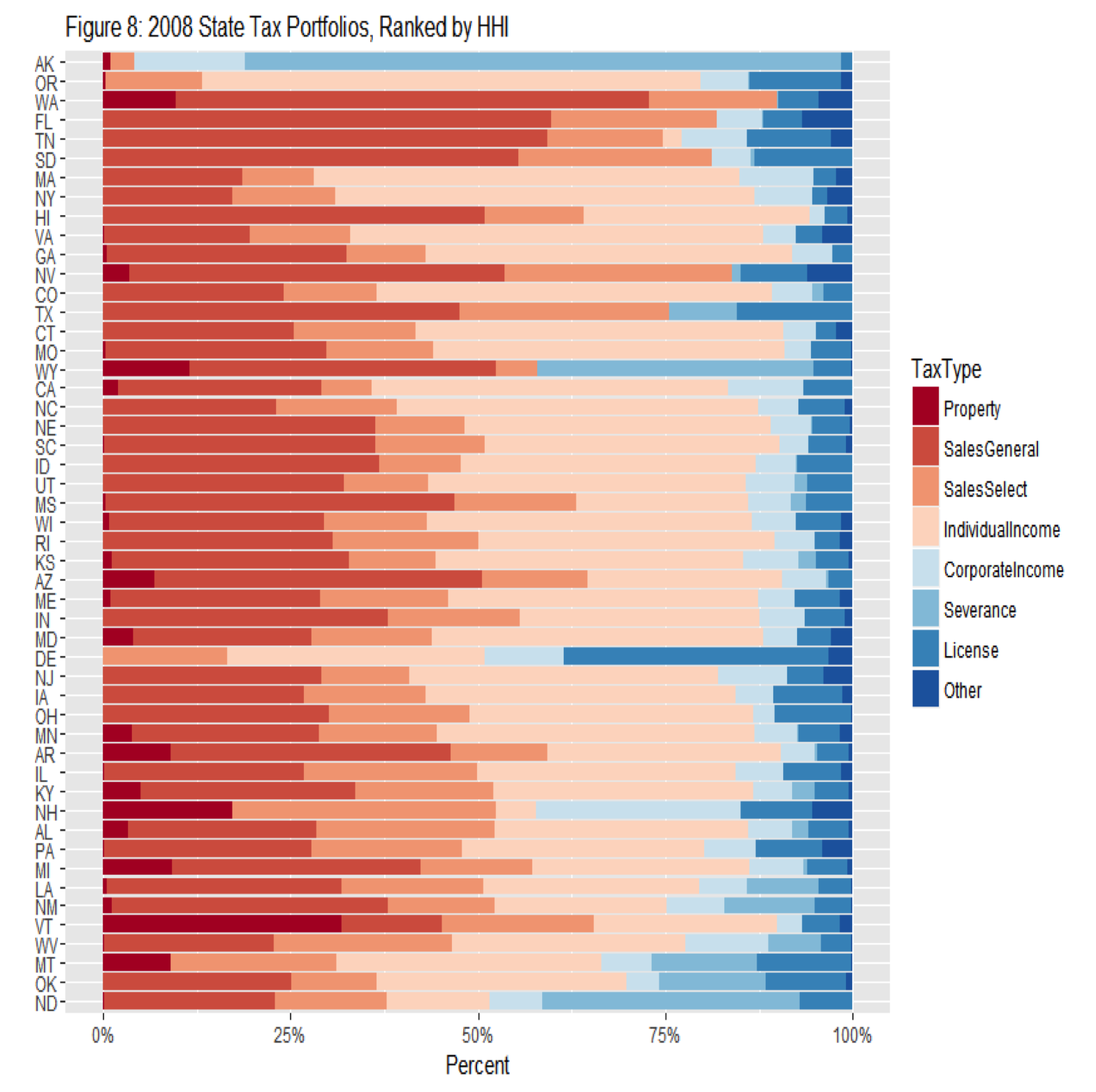

This figure shows the composition of each state’s tax portfolio in 2008 by tax type. CITes are represented in powder blue, personal income taxes (PIT) in light pink. Oregon’s CIT receipts as proportion of disposable income ranks 25th out of 50 states – right smack dab in the middle of the pack.[2] The most distinctive thing about OR compared with other states is its heavy reliance on the PIT – the fairest and most transparent of the tax types used widely by state governments.

Nor

is it true that Oregon has a “very low corporate tax rate.” Oregon’s statutory

CIT rate is above the national average. Nevertheless, there is no question that

CIT collections have lagged the growth in business profits over the past 40

years. That is true at the national level, it’s especially true at the

state level – and it’s true in Oregon as well. But it isn’t true

that once upon a time Oregon relied heavily on the CIT or that its decline has

impoverished Oregon’s state government.

In

Figure 8e, Oregon’s CIT is shown in light pink. The key takeaway from this

figure is that Oregon’s CIT never really played a dominant role in Oregon’s tax

system. Other revenue sources have always overwhelmed the CIT, both in terms of

totals and even annual fluctuations. The one thing that this figure doesn’t

clearly show is the decline of the CIT relative to other revenue sources. Figure

8g shows the composition of Oregon’s revenue portfolio over time. Again the CIT

is depicted by the light pink and it clearly tells a story of relative decline

– that, relative to Oregon’s portfolio of revenue sources, the CIT is only

about half as important as it once was. Figure 8g also shows that weight of ‘other

revenue’ and severance taxes in the state’s revenue system has fallen even

faster.

The Oregon Center for

Public Policy (OCPP) recently reported on the causes of the relative decline in

Oregon’s CIT. Their analysis is entirely accurate, although puzzlingly they list

the causes in reverse order of their importance. In a previous blog I

attributed Oregon’s CIT base erosion to the following: 58 percent due to the

U.S. tax code’s expanded pass-through provisions, 31 percent to corporate tax

sheltering and planning, and 11 percent to state-specific deductions,

exemptions, and credits. Ironically, IP28 directly affects C-corps, the only

business class that cannot avail itself of the U.S. tax code’s pass-through

provisions. It is also probably the case, although OCPP denies the possibility,

that a substantial portion

(1/2-2/3) of the CIT receipts lost to pass-through is recouped in terms of

higher PIT receipts.

Ultimately,

however, Our Oregon’s claim that Oregon’s C-corps

are not paying their fair share of taxes isn’t based on state CITs or even the

tax liabilities specific to C-corps. Rather their claims are based on the Anderson

Economic Group’s (AEG) 2016 State Business

Tax Burden Rankings report, which ranks states according to the remittances

of ALL businesses to state and local governments as a percentage of their pre-tax

gross operating margins – i.e., the sum of the Bureau of Economic Analysis’s

gross operating surplus measure plus ALL state and local sales, excise,

severance, property, corporate-income, and business-income tax payments,

license fees, and unemployment-insurance premiums.

That’s

a silly gauge, both from the standpoint of the numerator and the denominator. Mostly,

what the AEG report says is that the state of Oregon relies heavily on the PIT,

which is IMHO a feature, not a bug. Indeed, not all the items included in the

AEG report are taxes; some are fees for services rendered (UI premiums), but

AEG appears to arbitrarily include some charges and exclude others (most local

imposts, for example; these are relevant to us because Oregon’s are the highest)

in the US. More significantly, tax burdens don’t depend on who writes the

checks but on who suffers the consequent loss of buying power. Some of the

taxes remitted by businesses can be reasonably assumed to stick with their

owners (business income and corporate income taxes, mostly; property taxes,

probably); the incidence of the other taxes they remit is largely shifted

forward to final consumers (sales and gross receipt taxes) or backward to

employees (UI premiums) or other factor suppliers (severance taxes).

One

good thing about the AEG report is that it looks beyond state government,

recognizing that local taxes are part of the state system, even if they do so

in what I think is a wrong-headed and haphazard manner. In a future blog, I’ll

take a look at the claim made by supporters of IP28 that, as a result of

Measures 5 and 50, businesses in general and C-corps in particular are ducking

their fair share of Oregon property taxes.

[1]

They further say that Oregon “small businesses pay 8 times the tax rate of big

corporations.” Their reported source is the Department of Revenue, but I cannot

substantiate this claim one-way or the other. It is clearly not the case if one

looks only at the state’s CIT and business excise tax. They also claim that “[c]orporations with

more than $25 million in Oregon sales paying minimum taxes pay the equivalent

of only 3 cents for every $100 in sales,” citing the same source. Again, I can

neither confirm nor deny this claim, but it sounds credible, assuming that we

are talking only about the state’s CIT and business excise tax.

[2]

This would also appear to put paid to the claim that Oregon taxes corporations

at an unusually low rate “due in large part to the fact that most corporations

(72%) pay just the minimum, and those minimums are very low." In fact,

Oregon’s alternative minimum tax is the exception, not the rule. This claim looks

like question begging, pure and simple.

No comments:

Post a Comment